The price of specialty coffees & Fairtrade and organic certification

In an August 2020 report, an analysis is made of how the double Fairtrade organic certification influences the price of specialty coffees, based on data from the 2016/17 to 2018/19 harvests. The average New York price fell in those 3 seasons from an average of 1.40 to 1.01 USD/lb.

Of all the contracts in the 3 cycles, 26% have some certification and 13% of the contracts are FTO certified coffee, which represent 27% of the volume. Only Fairtrade coffee has a set minimum price and FTO has the highest minimum price at 1.90 USD/lb, including premiums.

The average FTO certified lot size was 27 thousand pounds, twice the size of non-certified coffees. The unweighted average price for FTO was 2.51 USD/lb versus 3.55 USD/lb for non-certified coffees, but the weighted average FTO price was 2.41 USD/lb versus a weighted average of 2.17 USD/lb for non-certified coffees.

Non-certified coffees get better prices for lots less than 40 thousand pounds and higher cup scores (84+). FTO generates a better price for lots of a whole container and cup 80–84, in addition to the guarantee of the minimum price of 1.90 in a market where the reference price fell from 1.40 to 1.01 USD/lb.

Specialty coffees & COVID-19

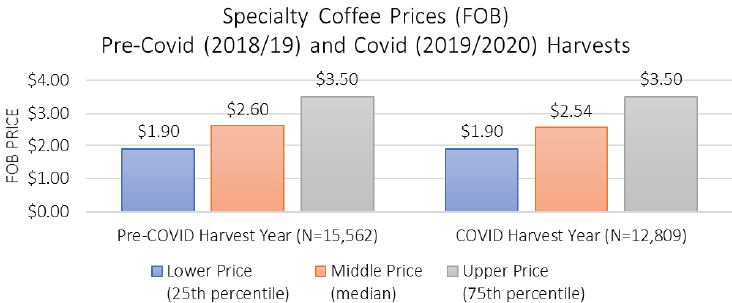

The impact of COVID-19 was first noted in a 5% drop in the number of contracts in 2019/20, possibly due to buyers’ fear of losing market with the closure of specialty coffee shops with high-quality coffee, but also because of the uncertainty regarding the offers. However, volume was down just 0.6% as average lot size was up 24% to 24,125 pounds.

Total value fell 1.9% to 309 million dollars. Cup quality (average 84.75 before, 84.51 after) and prices were practically the same. In the same range of 1.90–3.50 USD/lb, the average price fell from 2.60 to 2.54 USD/lb.

The volume of coffee with cup 80–84 rose 17.1% and that with cup 84+ fell 20.4%. There was a marked difference between Europe and the United States & Canada. In Europe the 80–84 cup rose 41.5% in volume and the 84+ cup fell 7.5%, in the United States & Canada the percentages were +12.5% for 80–84 and -29.1% for 84+.

One major change was the pricing. Before the pandemic, 75.7% of contracts had a fixed price, well above the price of the New York futures market, especially for coffee with a score of 84+. This advantage turned into a disadvantage when the pandemic began and it was possible to take advantage of the increase in both the New York price and the differentials for washed arabica, which normally go in the opposite direction, as we pointed out in The differential — Part 2.

75.7% was sold at a fixed price, thus not taking advantage of the double increase in the New York price and spreads from February 2020. The number of spread contracts with 80–84 cup rose sharply to 53.6% and the average size in this segment rose 30.6%. 58.3% of the contracts with the 80–84 ratio are certified against 19.1% with the 85+ ratio. This segment took more advantage of the price increase, which rose on average 0.14 USD/lb compared to before the pandemic.

Data for this analysis cuts to September 2020 and includes relatively little coffee from countries whose harvest begins in April-May. In order to assess the impact of COVID-19, the data from the 2020/21 cycle must be analysed.

In the last harvest, the number of contracts fell 6%, but the volume 37% and the value 22%, while the number of organizations that provided data rose from 90 to 103.

Specialty coffee and prices per country

The fourth edition of the guide also presents price data by continent (Africa, Asia, Central America & Mexico and South America), but it seems less relevant, because in the averages mix many things get mixed and the analysis is lost. Thus, in South America (median cup 85, batch 5,942 lbs and price 2.50) the extremes of Ecuador (cup 87, batch 772 lbs and price 4.75) meet with Brazil (cup 83, batch 35,965, price 1.60, which seems to be the minimum price Conventional Fairtrade for washed coffee). In Asia (cup 84, lot 29,762 lbs, price 2.40) East Timor and Papua New Guinea dominate (cup 83 / 84, both lot 39,684, which is the largest sample size, and price 1.90, which seems to be the Fairtrade minimum price organic).

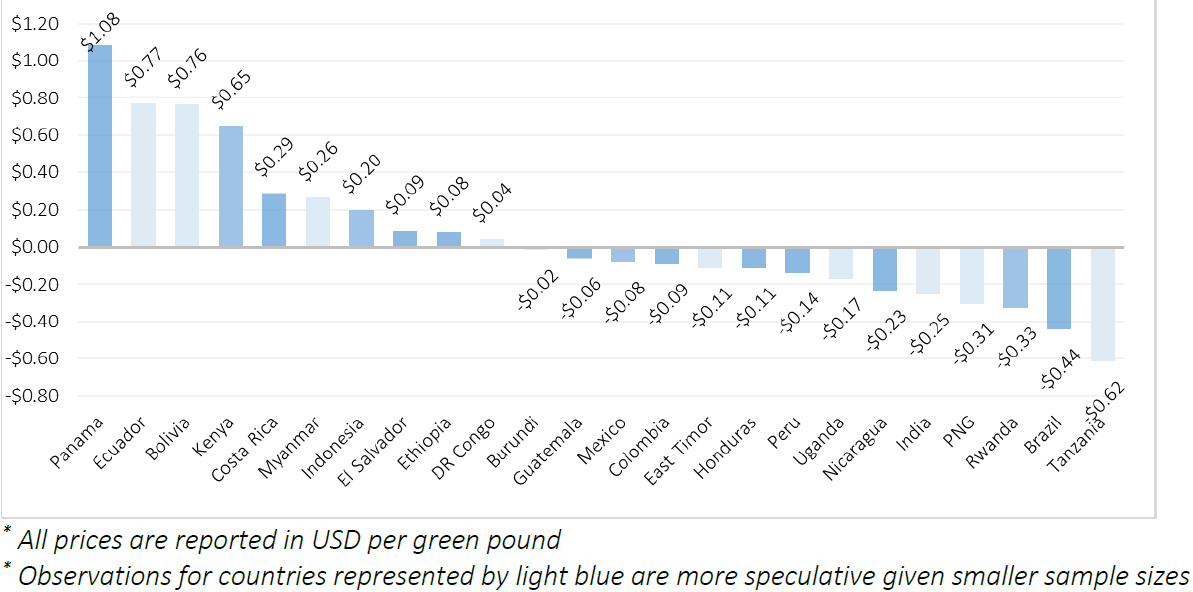

More interesting then to do the analysis at the country level. The average price ranges from 1.60 for Brazil to 7.50 for Panama (average size 608 lbs, the smallest) and an average cup of 82 for Nicaragua, up to 87 for Ecuador. Given the variability in price, cup and size by country, a formula is applied to correct the price per cup and size to the data for the last 3 years. The result is a correction of the price by country, which allows comparing the countries, which is presented in the following graph:

Conclusions

In their conclusions, the authors state that with these data, buyers and sellers can calculate how much a coffee should cost. Thus, a container of 40 thousand pounds or more of coffee from El Salvador with a score of 83 has a reference price of 2 USD/lb (average price in 2020/21 for that size and cup), plus an adjustment of 8 cents for El Salvador. 2.08 USD/lb. In the same way, a batch of 2 thousand pounds of 87 cup coffee that has an average price of 3.70 USD/lb in 2020/21, should have a discount of 6 cents for Guatemala and have a reference price of 3.64 USD/lb.

Here the guide missed its target. Presenting price references per cup and lot size is very useful, but believing that a reference price can be calculated statistically with a correction by country is far-fetched. For this, important factors are missing, such as the buyer-seller relationship, consistency in quality and service, the attributes that the coffee has (cup profile is more than just a score), the history of the people behind the coffee, traceability and many more.

These are not so easy to quantify, but it is worth collecting information of that type in future editions. In a way, it is already mentioned in the topics that are to be examined in the future and that include other quantitative and qualitative variables that influence the price.

For the next edition with the data for the 2021/22 harvest, it will be necessary to consider when the coffee is harvested and sold, because as of July 2021 the price on the New York futures market began to rally to up to 260 cents in February 2022. Where the harvest begins in April — May, a lot of coffee will have already been sold before the price increase and those who took the most advantage of the high prices will have been those who sold between November 2021 and February 2022, which is the main harvest time in the northern hemisphere.

Get the latest resources, trends and stories for coffee professionals in your inbox. Sign-up for the monthly Beyco newsletter.